Gaap Depreciable Life Of Solar Panels

Week 4 Cfa Level Ii Key Differences Between Us Gaap And Ifrs Part I Youtube Cpa Exam Accounting Financial Ratio

20 2 Financial Reporting Considerations Related To Covid 19 And An Economic Downturn March 25 2020 Last Updated September 18 2020 Dart Deloitte Accounting Research Tool

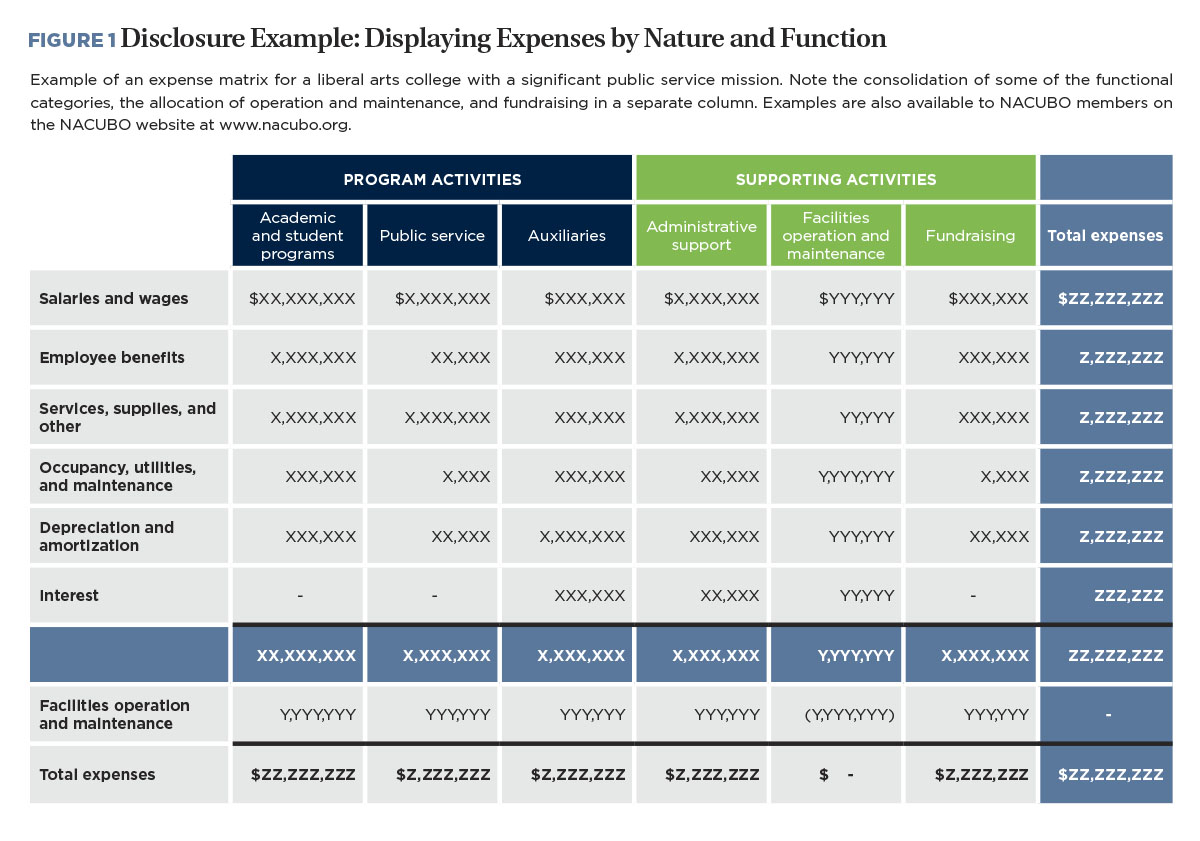

Putting New Rules Into Practice Business Officer Magazine

Pdf Big Gaap Little Gaap Will The Debate Never End

Types Of Accounting Accounting Government Accounting Cost Accounting

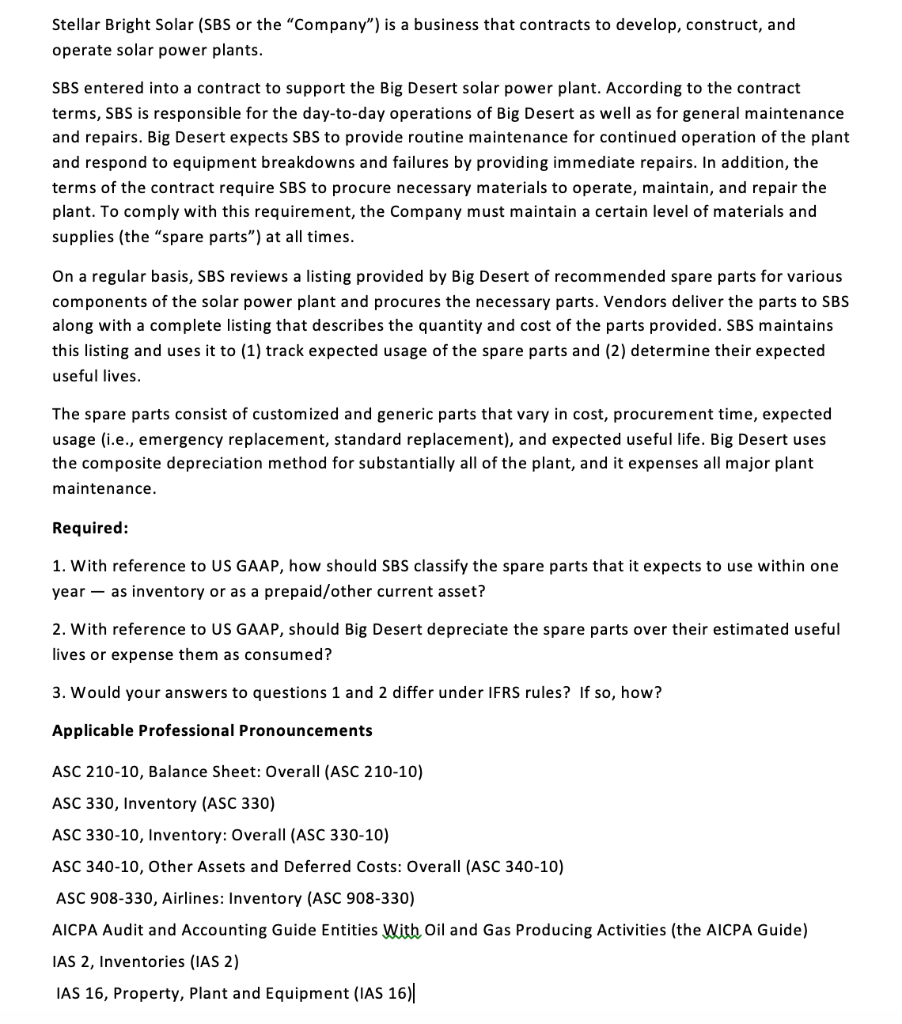

Solved Stellar Bright Solar Sbs Or The Company Is A B Chegg Com

This greatly enhances your ability to recover the costs from your solar investment.

Gaap depreciable life of solar panels.

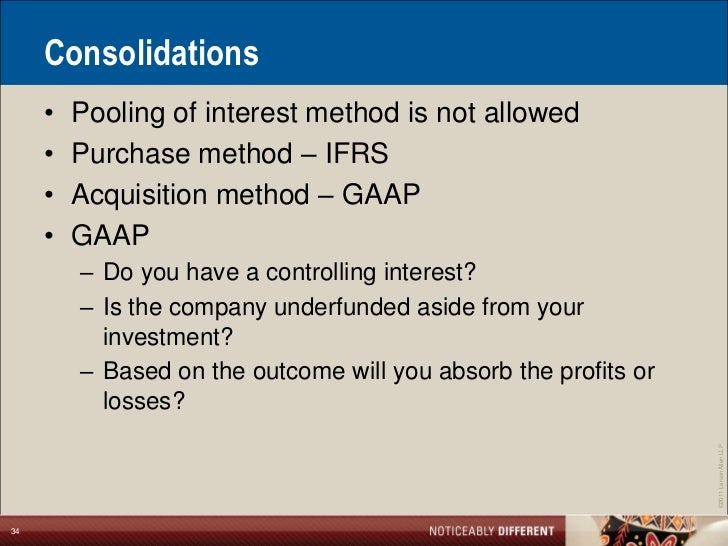

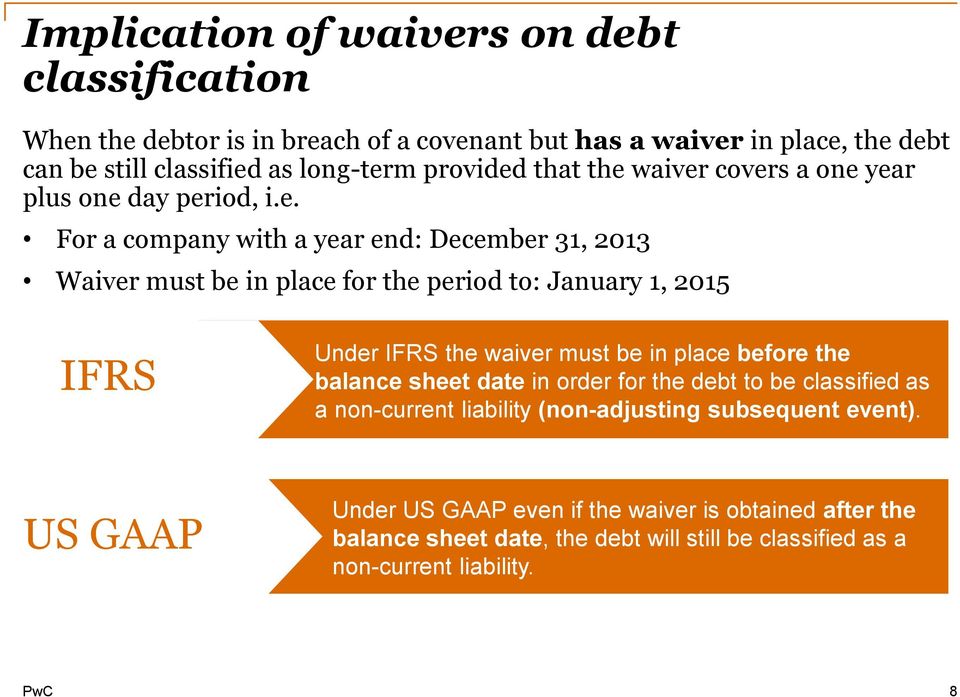

Ifrs Vs Gaap

Accounting Practitioners Guide For Renewable Energy Projects Pdf Free Download

Us Gaap And Ifrs Accounting And Reporting Issues For Shipping Companies Reminders And Updates Pdf Free Download

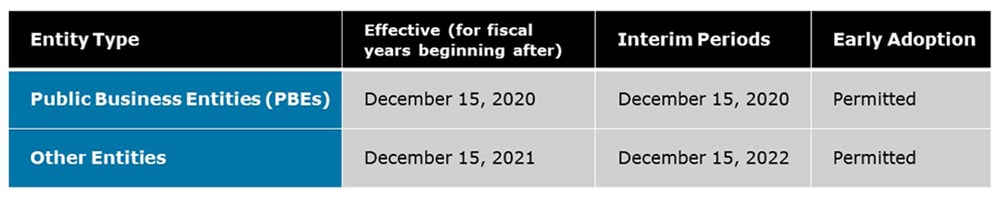

Fasb Issues Update To Insurance Accounting Standard Blog Deloitte Us

Source : pinterest.com